Blog Post by Yari

January 28th, 2026

Totally Spies, Portfolio, & Stress Testing

Three agents. One mission. A sleek control room hidden behind a high school hallway, in not creepy way.

If you grew up watching Totally Spies, or just super into campy 2000’s cartoons like me, then you already understand stress testing.

If your new to the cartoon scene, Totally Spies is where the TikTok audio for “Oh my gosh! She’s bald! She’s bald and she’s torturing people who have hair!” comes from.

Before Clover, Sam, and Alex ever stepped into the field, someone had to run the simulations. You as an analyst can do this using real historical data, and even simulated data.

You can then ask real questions that the girls were constantly encountering:

- What happens if the villain hijacks global infrastructure?

- What if gravity reverses?

- What if the plane fails halfway through and the gadgets stop working?

Only they didn’t wait to be surprised… because they tested scenarios when they trained.

Finance works in a similar manner, except most portfolios are sent into the field with zero rehearsals prior.

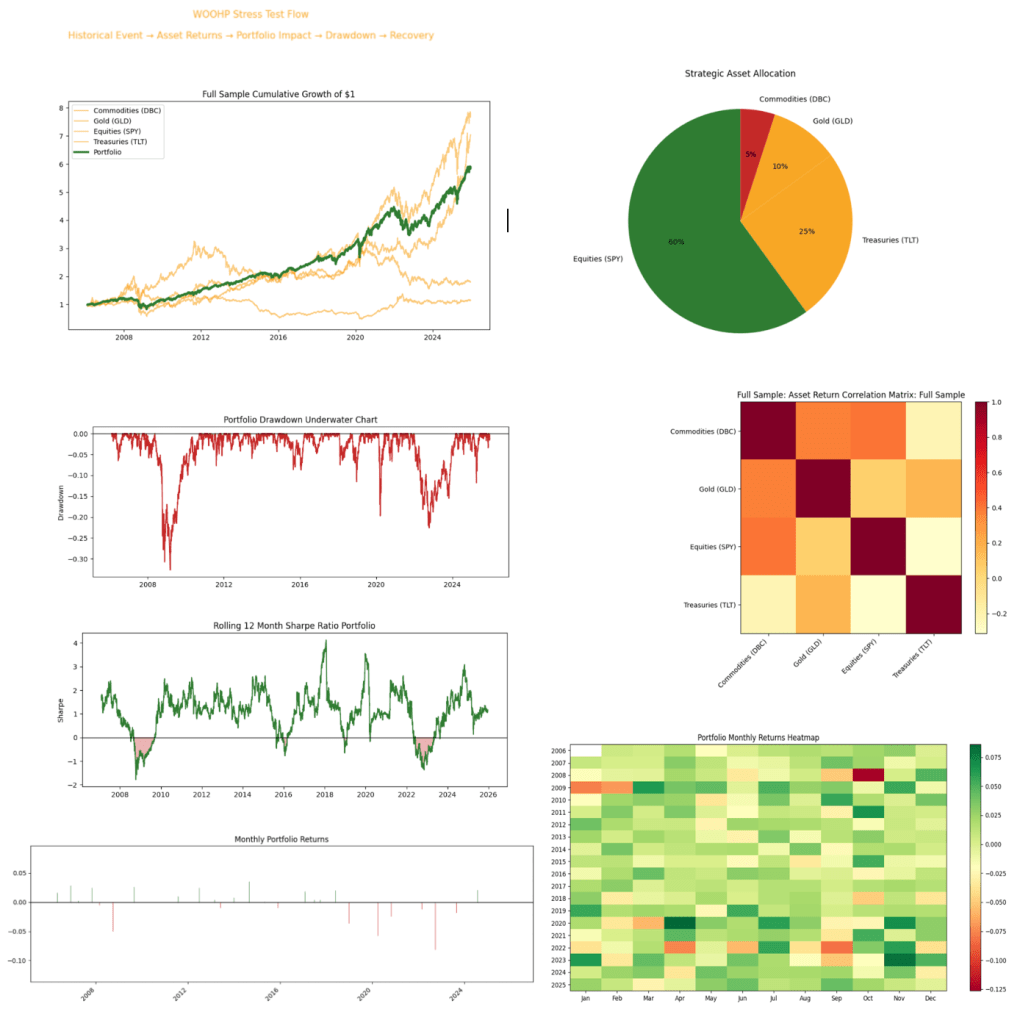

Here at the Yariverse, we love clean back tests. Smooth equity curves. Annualized returns that look good in isolation. All about that Beta and Alpha life.

But markets don’t move that politely, like ever.

It’s a problem if they do, because markets lurch, freeze and even sometimes break correlations. They can spike rates overnight and wipe out assumptions that you didn’t even realize you were making.

That’s where scenario and stress testing become vital in finance and on any mission the girls in the show encountered. It’s not to predict the future, it to understand how fragile your portfolio becomes when things stop behaving or suddenly go upside down.

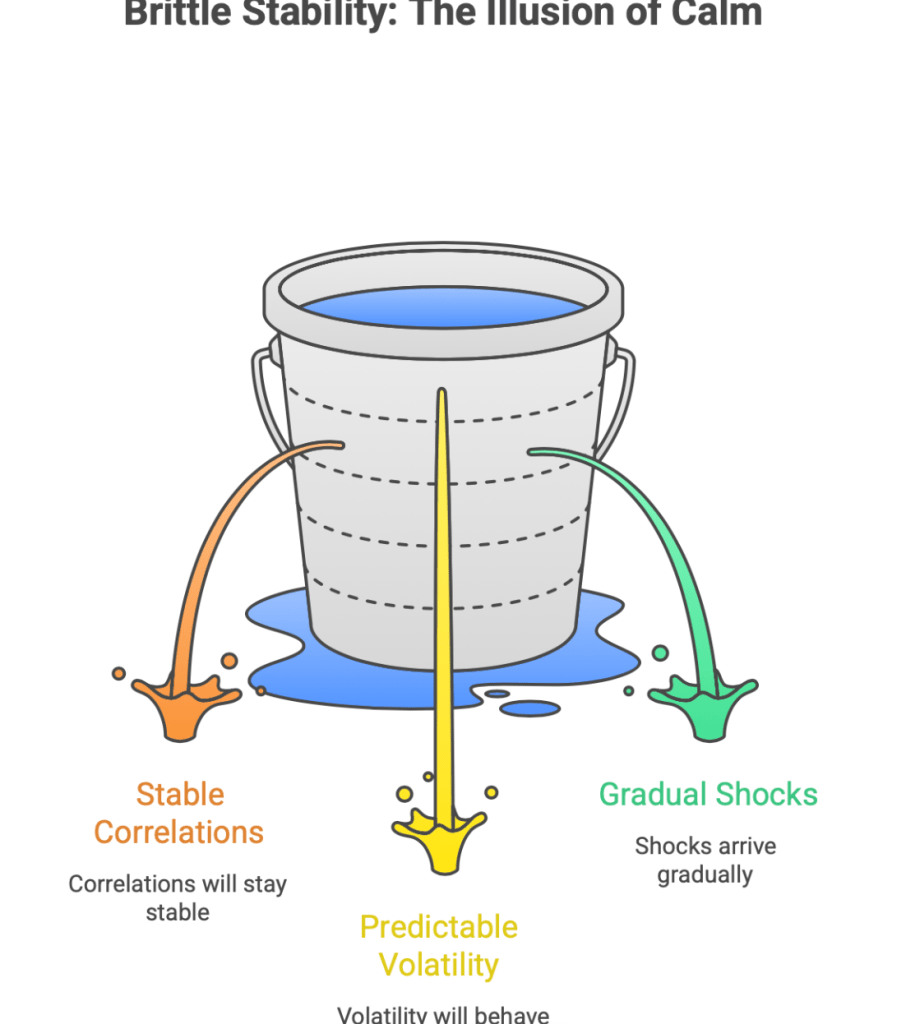

So, here’s your most import totally spies spy rule: never trust a calm room

In Totally Spies, a quiet control room was never a good sign, literally it was bad. Calm usually meant something was loading in the background and it was never in a good way for the girls or any NPC.

A portfolio that looks stable in normal conditions can be dangerously brittle under stress, like the student in Bio Lab that got all A’s but during practice but vomited at the first sight of organs during rat dissection. That’s because the most traditional metrics quietly assume that:

- Correlations will stay and remain stable.

- Volatility will behave.

- and that shocks arrive gradually instead of all at once.

Much like any of the villains in the show, markets don’t ask for permission.

Rate hikes don’t care about your sharpe ratio, or even if you used a cute pink glittery gel pen to get that answer by hand.

Instead, in finance stress testing answers a different question than backtesting: “What happens to me if the world breaks in a specific way?”

Just like in Totally Spies, we’re not testing for elegance or cute fits that I wish were real, no, we’re testing for survivability.

The villains (aka the scenarios that already happened)

In this model, we don’t invent cartoon chaos, but we do enjoy a good totally spies episode with milk and cereal. So, to make this more actuate to events, we’ll use historical villains in finance, the ones that already proved what breaks first in the real world:

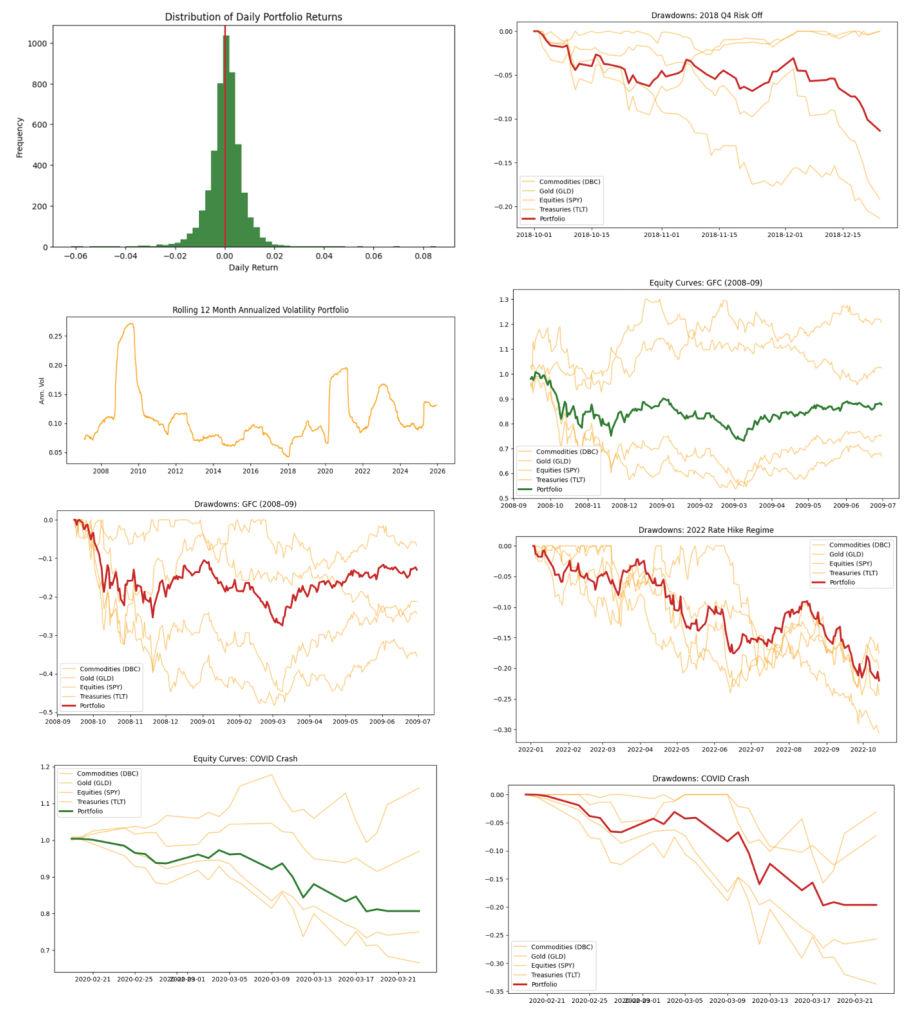

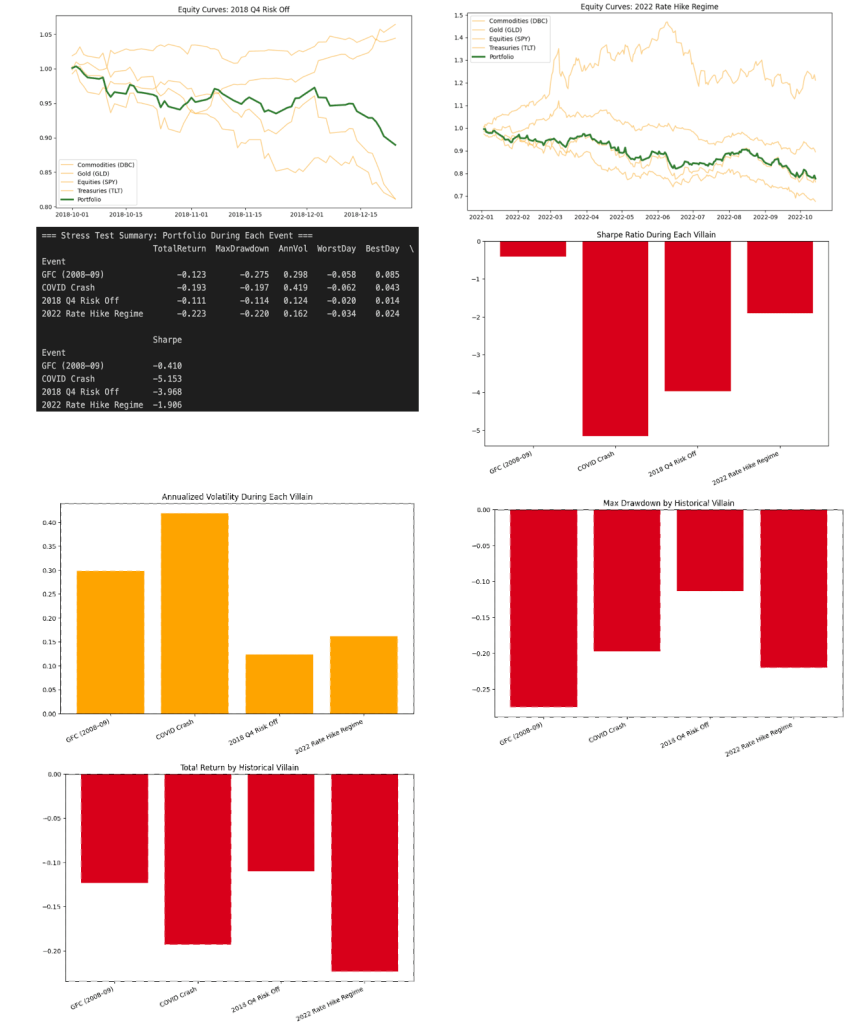

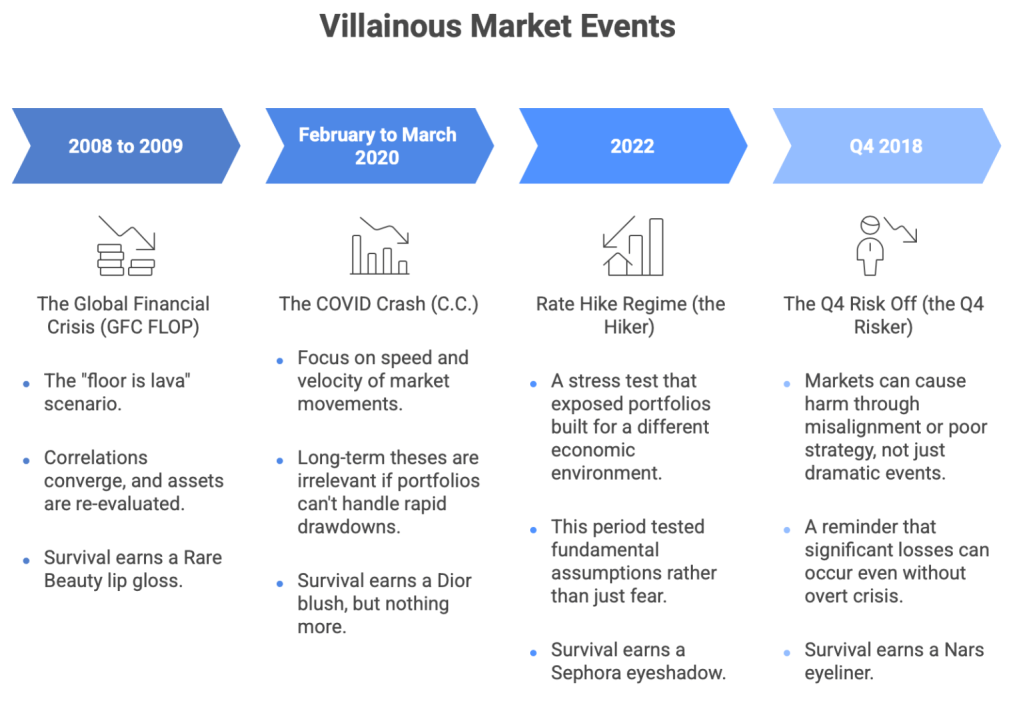

Villain 1: The Global Financial Crisis (2008 to 2009) aka GFC FLOP

This is the “the floor is lava”.

Liquidity vanishes, equities collapses. Fear becomes systemic. Correlations converge. Defensive assets finally show whether they’re real protection or just branding.

If your portfolio survived this, it earned its badge. You can get to buy yourself a cute Rare Beauty lip Gloss.

Villain 2: The COVID Crash (February to March 2020) aka C.C.

This is all about speed.

Everything drops at once without warning. Diversification disappears temporarily. Markets reprice the world in weeks, sometimes even less with days. If your portfolio couldn’t handle velocity, your long term thesis didn’t matter one bit.

This taught that drawdowns aren’t just depth, they’re about “how fast you panic.”

If your portfolio survived this, it earned its badge. You get to buy yourself a cute Dior blush but nothing more.

This is villain no one dressed for.

Villain 3: The 2022 Rate Hike Regime aka the Hiker.

Stocks fell. Bonds fell even worse. The comfortable assumption that “bonds will save me” quietly failed. This was the stress test that exposed portfolios built for a zero rate worldwide. If 2008 tested fear, then 2022 tested assumptions.

If your portfolio survived this, it earned its badge. You get to buy yourself a cute Sephora eyeshadow.

Villain 4: The 2018 Q4 Risk Off the Q4 Risker

No recession, or crash headline. Just policy uncertainty, positioning, and tightening liquidity. This is the reminder that markets don’t need drama to hurt you. Sometimes the villain is simply misalignment or a terrible haircut.

If your portfolio survived this, it earned its badge. You get to buy yourself a cute Nars eyeliner.

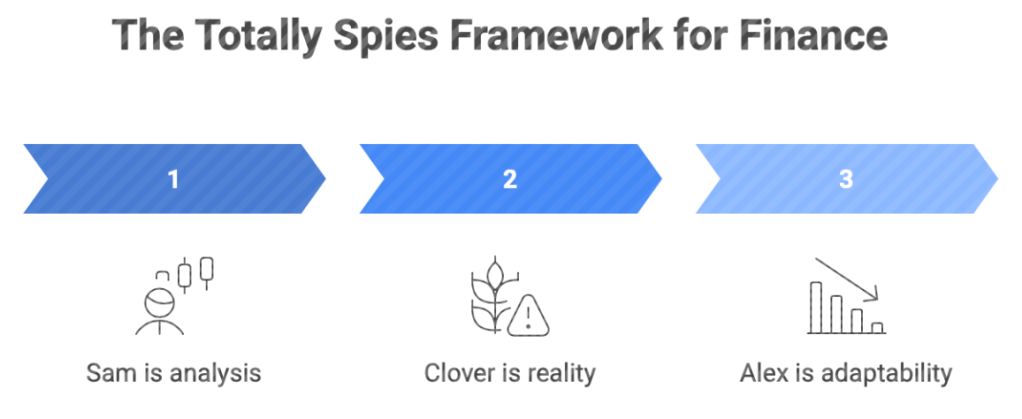

The Totally Spies framework but make it finance

Each spy had a role, and so does your portfolio framework.

- Sam is analysis, which covers: Expected returns, correlations, assumptions, factor exposures.

- Clover is reality, which covers: Panic, drawdowns, style breaks, correlations going to one.

- Alex is adaptability, which covers things like: Can the portfolio survive, rebalance, and recover? Yes? no?… Maybe is simply not enough.

Scenario testing is your control room. So, you won’t panic mid mission.

In finance this is where you’ll calmly watch outcomes before capital is deployed. Relax, sit back, you only get champagne if your portfolio survives.

Why this matters more than optimization?

Optimization asks the following: “What portfolio looks best under average conditions?”

While Stress testing asks the following: “What portfolio doesn’t utterly destroy me when conditions are abnormal?”

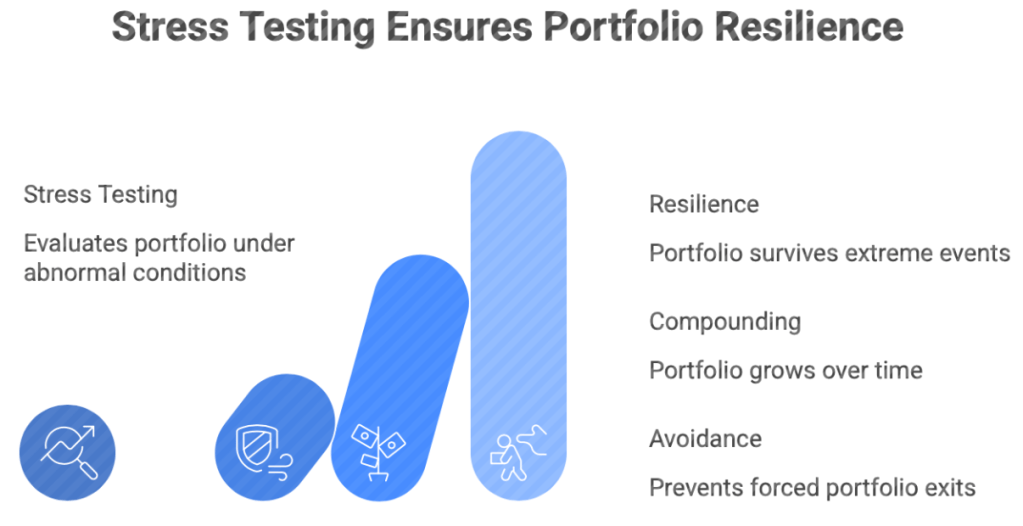

Remember, high performers don’t optimize for comfort, they optimize for resilience.

A portfolio that survives stress can compound later.

A portfolio that breaks, much like a terrible date, doesn’t get a second chance.

Losses are the entry fee.

Forced exits are the failure. You never want to leave on someone else’s terms, ever.

Remember

Markets don’t reward bravery without preparation.

Scenario testing isn’t pessimism, it’s actually intelligence. If you strategize the correct models. Stress testing is all about choosing awareness over surprise.

If Totally Spies taught us anything, it’s this:

The mission isn’t to avoid danger, it’s to enter it informed. Hence the debriefings, and pretested gadgets.

Before you send your portfolio into the world, ask:

What if equities drop 30%? What if rates jump 200 basis points? What if diversification fails exactly when I need it?

Because if you don’t run the scenario, the market will, and it won’t ever brief you first.

Here’s a quick code.

Here’s what your output should look like: